by François Masquelier, Head of Corporate Finance and Treasury, RTL Group, and Honorary Chairman, EACT

When you talk about collateral, treasurers often bridle, worrying that they will be required to meet systematic margin calls. This discussion recently moved to OTC (over-the-counter) derivatives, which we know will need to involve margin calls in the future, unless exemption is given to non-financial companies (which seems to be the case). This collateral market today represents a few hundred billion euros under management. However, this market has a number of imperfections and a degree of inefficiency that are giving rise to operational problems. There are also market restrictions which prevent the banks, certainly, from making the best use of collateral. The idea we start from is, however, simple: why not use the assets that you hold to finance yourself or, in less favourable economic circumstances, accept them in order to bolster your own position? Collateral can be used for various reasons such as (1) margin calls on derivative product transactions; (2) as security for financing with market counterparties or central banks; (3) dealings with clearing houses or central counterparties (CCPs) and (4) for settling transactions.

Repo or not repo?

Repurchase agreements, often referred to as repos, involve the sale of assets under an agreement or contract enabling the seller subsequently to buy them back. The buyback price will be higher than the initial price, with the difference representing interest calculated on the basis of the repo rate. The buyer of the securities is the lender (’giver’) and the seller is the borrower (’receiver’). The collateral is reassurance for the lender and serves to safeguard its assets. It boils down to a cash transaction combined with a forward transaction and, at the end of the day, can be likened to a secured loan.

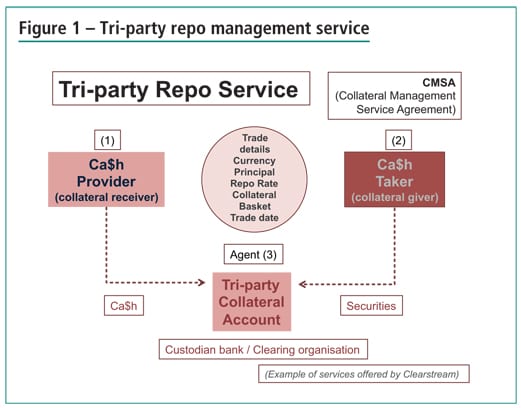

The characteristic of a tri-party repo is that there is a custodian bank or an international clearing organisation between the two parties. This third party plays the role of agent or intermediary, handling the transaction’s administration, including the allocation of the assets pledged as security. Examples of these intermediaries are J.P. Morgan, Bank of NY Mellon and Clearstream in Luxembourg. In return for this tripartite agreement, the intermediary provides a management service including the profile of the eligible collateral. This enables the buyer to define its risk appetite and, to a greater or lesser extent, gives it the ability to sell its assets in the event of problems.

Sign up for free to read the full article

Register Login with LinkedInAlready have an account?

Login

Download our Free Treasury App for mobile and tablet to read articles – no log in required.

Download Version Download Version

")

")

")

")

")

")

")