by Jim Fuell, Managing Director, Head of Global Liquidity, EMEA, J.P. Morgan Asset Management

Separately managed accounts can provide an attractive alternative for treasurers looking to generate higher yields on their excess cash than are available from money market funds. In this article, Jim Fuell discusses how these accounts can be tailored to meet specific risk and return objectives, giving treasurers not only the potential to earn more on their cash, but to exercise greater control over what they invest in and their investment horizon.

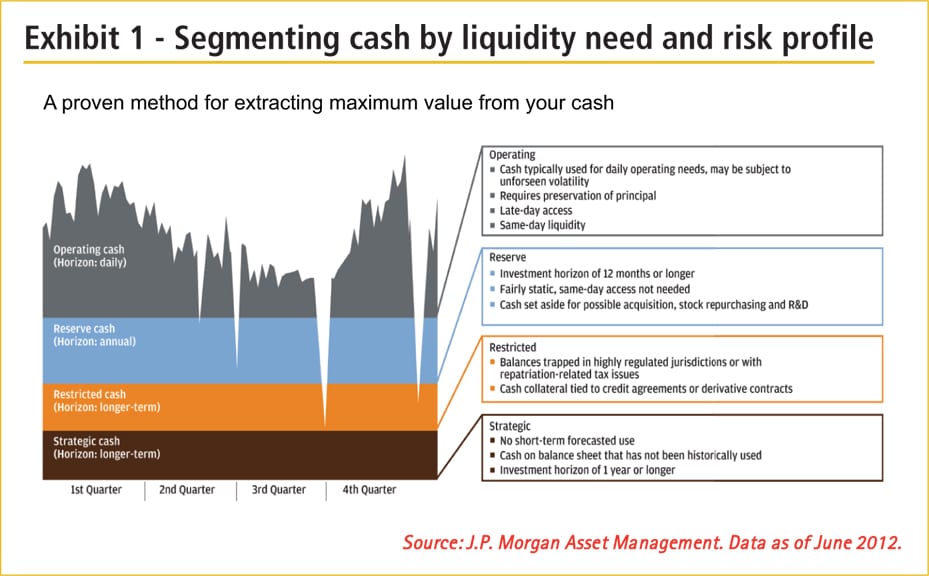

Broaden your investment horizon

While treasurers in the US have been using separately managed accounts for some years, only recently has their popularity grown in Europe. During the credit crisis, the priorities for many European treasurers were to preserve capital and ensure significant liquidity to meet business needs. However, today, many companies are flush with cash and do not have the same restrictive liquidity requirements. The protracted period of low interest rates and exceptionally low money market fund yields has further encouraged companies to broaden their search for additional yield, while still remaining relatively risk averse.

Separately managed accounts invest in individual securities on behalf of a corporation, insurance company, pension fund or various other institutional investors. As separate accounts are tailored to meet an investor’s risk appetite, yield target and liquidity needs, the expected investment return can be larger when compared to other short-term investments such as money market funds or bank deposits. Conventionally, aiming for higher returns requires investors to assume additional risk, therefore making separate accounts suitable for cash balances that are not needed for at least six months. The cash amount should also be higher compared to a money market fund investment to ensure adequate diversification is achieved in the underlying securities.

Click to enlarge

Sign up for free to read the full article

Register Login with LinkedInAlready have an account?

Login

Download our Free Treasury App for mobile and tablet to read articles – no log in required.

Download Version Download Version")

")

")

")

")

")

")