by Eben Maré, Head of Absolute Return Funds, Stanlib, and Chris Holdsworth, Quantitative Strategist, Investec Securities

Real interest rates have been negative in the US following the 2008 sub-prime crisis. A similar experience holds in many countries, including emerging markets such as South Africa. If we follow recent guidance from the US Federal Reserve it is clear that this situation is set to change given the end of the so-called Quantitative Easing 3 monetary policy stimulus programme, although the timing is uncertain. We investigate the effect of real interest rates on equity performance.

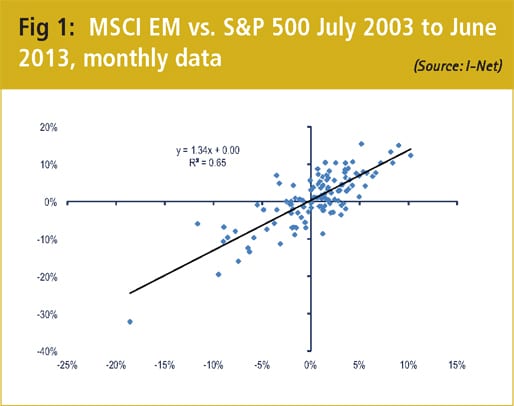

At face value emerging equity markets are simply a play on the performance of the S&P 500 index. If we perform a linear regression analysis of monthly MSCI Emerging Market (MSCI EM) returns vs. S&P500 returns over the past ten years we find a beta of just over 1.3 with a respectable R2 value as indicated in the graph below.

For any given positive expectation of returns for the S&P 500, the expected return for the MSCI EM in USD should be greater to compensate for the greater systematic risk inherent in investing in emerging markets.

Sign up for free to read the full article

Register Login with LinkedInAlready have an account?

Login

Download our Free Treasury App for mobile and tablet to read articles – no log in required.

Download Version Download Version

")

")

")

")

")

")

")