- Livia Benisty

- Chief Business Officer, Banking Circle

Despite rapid digitalisation of global e-commerce, many online merchants still face payments barriers when it comes to expanding internationally. Banking Circle’s latest research into this dynamic topic highlights how payments businesses can utilise partnerships to improve the cross-border offering for their underlying customers.

Over the past two decades, digitalisation has accelerated the development and broadened the reach of businesses and customers to the point where online channels now matter to merchants more than physical shops. This has made cross-border trade significantly easier. Global e-commerce has broken down barriers and created a truly global digital marketplace. However, the high cost and slow transfer times of cross-border payments mean many sellers and merchants remain unable to access international markets.

The reality is that while SMEs accelerate their digital transformation, some of their partner banks and payment service providers (PSPs) struggle to tackle issues such as the cost and speed of cross-border payments, high fees, and the delivery of lower-risk transactions. Legacy technology and the correspondent banking model make it difficult for FIs serving merchants to deliver more affordable, accessible cross-border payments. The growing threat of de-risking only adds to the difficulties.

Since the 2008 financial crash, banks have had to protect themselves by avoiding higher-risk clients, and many have opted to carry out wholesale de-risking to avoid potential risks from entire regions or sectors. Consequently, many businesses and smaller banks cannot find suitable, affordable partners for non-core services including cross-border payments.

In 2021 Banking Circle spoke to 700 European banks, fintechs and PSPs, about the threats their businesses faced at that time. The study found that 77% of these FIs have increased the number of correspondent banking partners they have in the past 10 years to mitigate against being de-risked.

In 2022 we spoke to 900 European merchants selling online to discover their current expectations of payment partners, and what their providers are doing to deliver better solutions.

The challenges FIs face and the expectations of their merchant customers are the subject of this article.

To remain competitive and increase ‘stickiness’, PSPs are increasing the range of added-value, non-core solutions they provide.

New solutions to serve a new landscape

SME merchants have shifted to online with just 34% of those Banking Circle surveyed using a physical outlet for sales. A significant 49% use online marketplaces, 46% their own website, and 39% harness social media as their sales channel. And merchants have a wide range of requirements and priorities with respondents confirming they currently work with an average of three PSPs in order to meet the needs of their business and change PSPs every two years.

More than 36% of merchants use more than one PSP to access different benefits; 37% utilise more than one PSP to enable them to serve different geographies. One third (33%) operate with more than one PSP to mitigate against being de-risked. But for 34% of the merchants we surveyed, the choice of PSP is dictated by the marketplace they use, leading to a higher number of PSP partners.

To remain competitive and increase ‘stickiness’, PSPs are increasing the range of added-value, non-core solutions they provide. Marketing assistance was cited as a key benefit for 34% of merchants surveyed; direct debit for 31% and the ability to pay EU and UK VAT via their PSP for 31%.

Other payment solutions were also seen as value-adding options, including request to pay (RtP) for 30% and buy now, pay later (BNPL) for 28%.

Smaller companies found marketing support (39%) and RtP solutions (50%) the most helpful services. This enthusiasm for RtP reflects the wider need for small firms to receive payment quickly, as such software often features automatic invoicing and reminders, cutting down on the administrative burden.

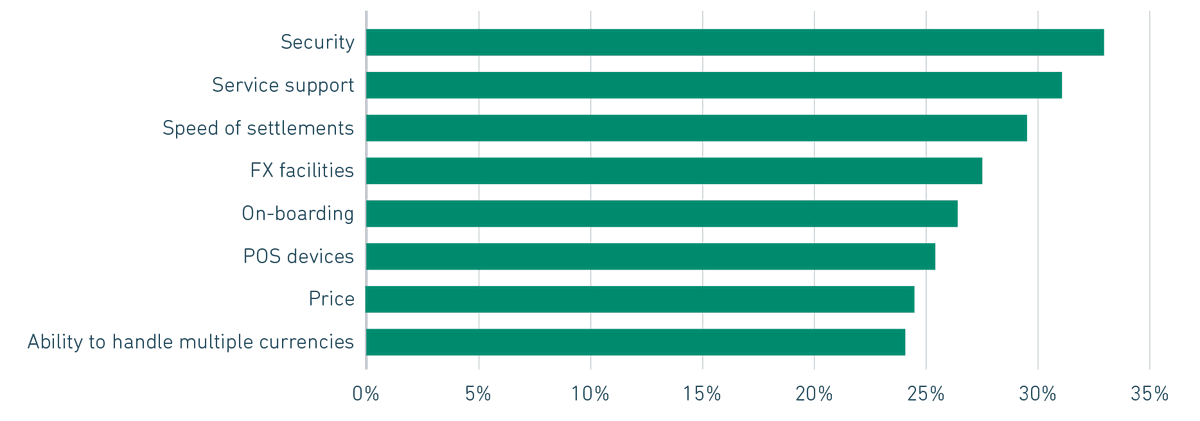

FIG 1: PAIN POINTS PERSIST: SECURITY PARAMOUNT

Source: Censuswide/Banking Circle

Tackling pain points

Of the four biggest pain points the merchants surveyed experienced with their PSPs, two relate directly to cross-border payments.

When Banking Circle asked merchants how their PSP partners performed in the areas of cost of transactions, reliability, and speed of settlement, there was a generally positive response. Looking at cost of transactions, reliability (rarely offline), security, 24/7 support, and speed of settlements, in each area around one in three merchants felt the performance of their PSP was quite good.

24/7 support was the poorest performing area, with 23% choosing ‘poor’ or ‘very poor’. Security scored highest, with 21% selecting ‘very good’.

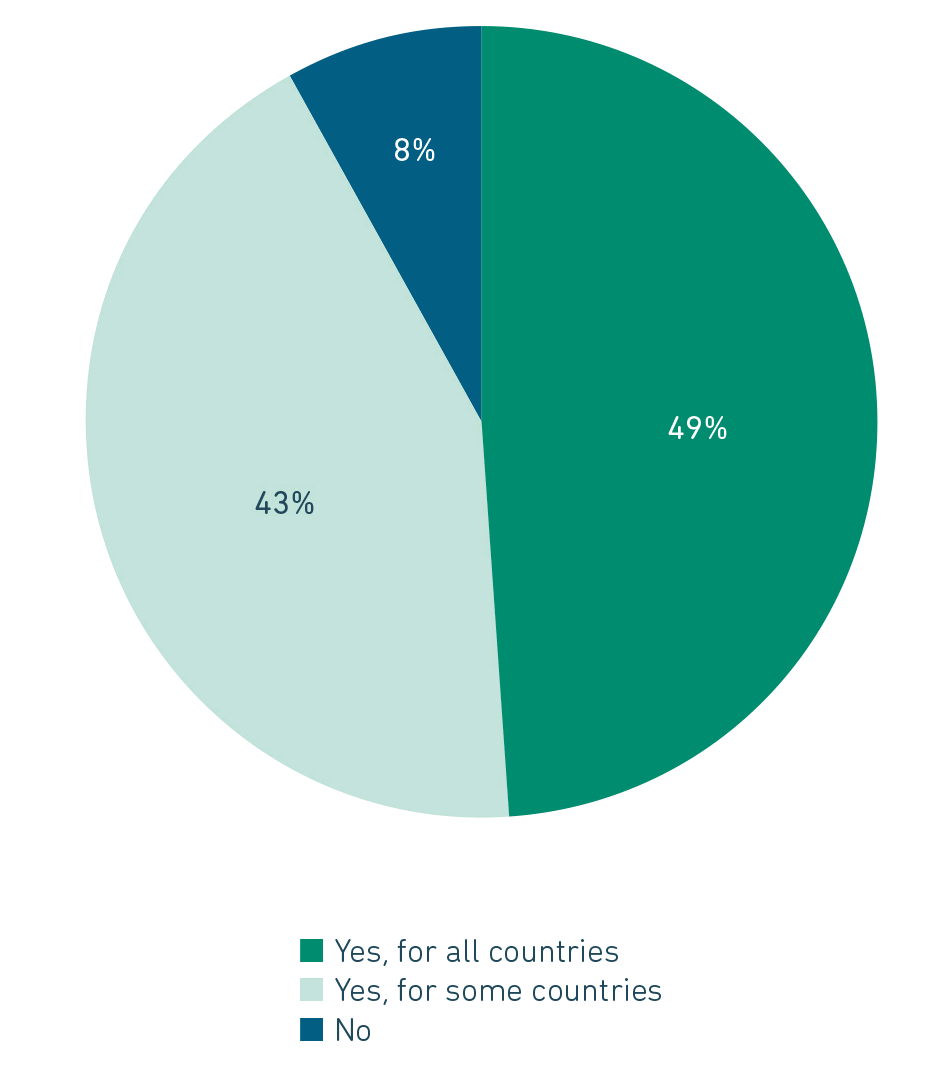

Merchants are also looking for more support regarding regulatory requirements overseas. Less than half (49%) said they receive assistance from their PSP for every country in which they trade, with 43% receiving support in some countries.

FIG 2: REGULATORY SUPPORT NEEDS TO GO GLOBAL

Source: Censuswide/Banking Circle

Utilising the ecosystem, not going it alone

Banking Circle’s data shows that PSPs offering access to a suite of solutions and added-value propositions in one place will be an attractive option, helping to simplify payments for the merchant. And the wider range of benefits offered by a PSP, the more payments will be sent their way. However, PSPs cannot build and maintain a broad enough suite of solutions and services working in isolation.

Working in tandem with external expert partners addresses the challenge, delivering market-leading solutions underpinned by fit-for-purpose tech and supported by regulatory expertise.

Banking Circle welcomes and indeed invites discussion on the points raised in this recent research, and looks forward to working in collaboration with the industry to overcome hurdles, realise the promise of digitalisation and deliver a fairer, more accessible, and inclusive economic future.