- Aoife Wallace

- Head of Trade & Working Capital Europe, Barclays

- Daniela Eder

- Head of Payments & Cash Management Europe, Barclays

Covid-19 has changed so many aspects of life and business – global trade is no exception. With trade flows declining, and commercial payments following suit, Aoife Wallace, Head of Trade & Working Capital Europe, Barclays, and Daniela Eder, Head of Payments & Cash Management Europe, Barclays, examine how treasurers can play their part in supporting the recovery – from financing their supply chain partners to digitising trade and cash management workflows.

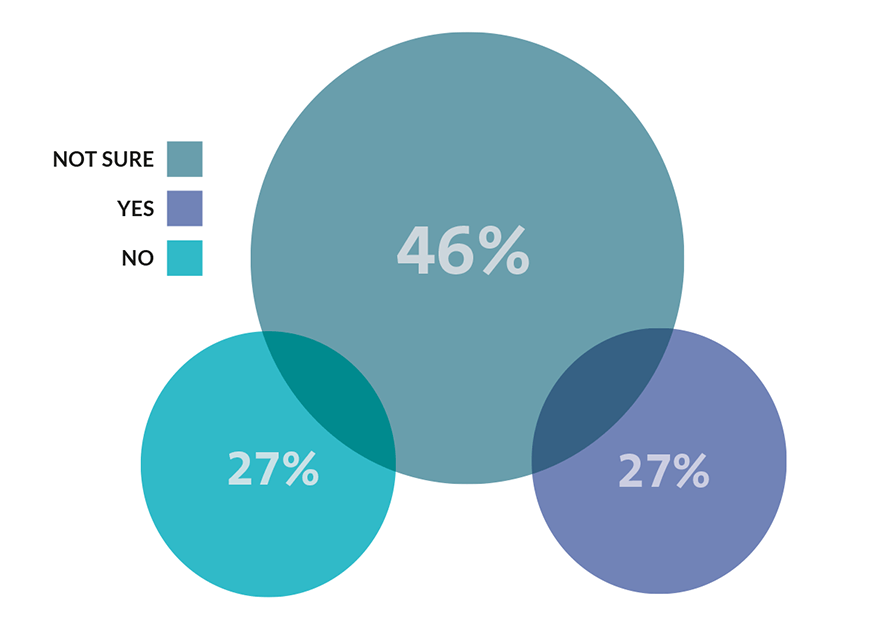

Even before the term ‘Covid-19’ was on the lips of treasurers across the world, challenges to the future of global trade and supply chains were looming. International trade tensions, coupled with ongoing Brexit negotiations, not to mention the upcoming US Presidential election, were all causing ripples. In turn, this uncertainty was impacting corporates’ requirements for trade- and supply chain finance (see fig. 1)

Fig 1: Need for increased trade and working capital facilities in 2020 |

Inevitably, this is impacting other areas too: Eurozone GDP for Q2 2020 shrunk by 15% year-on-year [2], for example. Commercial payments have also been significantly stunted due to the drop in trade. Eder comments: “Although e-commerce has risen enormously during lockdown as businesses have embraced new business models, Eurozone commercial payments for Q2 2020 were down 11% – according to data issued by SWIFT in August 2020 – and this is closely linked to the drop in trade. Likewise global commercial payments flows dropped by 10% during that same window.”

Smart financing solutions

While small green shoots of recovery are starting to emerge, the overall decrease in trade flows – combined with pre-existing geopolitical tensions – is a significant challenge for businesses, not to mention the global economy. Eder comments: “Companies have found that, even if they are surviving the crisis, their suppliers may be at risk. We have heard anecdotal evidence of large corporates offering financing to their suppliers during the Covid-19 crisis, simply to help those suppliers keep their heads above water, and to maintain the security of the overall supply chain.”

Wallace echoes this, adding that: “Supplier finance used to be primarily about looking at your own balance sheet as a buyer, and extending out payment terms as far as possible to reduce the cash conversion cycle. Now it’s being used as a tool by corporate buyers to help their suppliers survive the crisis, maintain the integrity of their supply chain, and drive long-term sustainable relationships.”

Today’s treasurers need to look holistically at their underlying supply chain and ensure the correct level of funding is in place throughout, in order to ensure resilience, believes Wallace. “Corporate buyers can no longer concentrate only on their top ten suppliers to the detriment of smaller suppliers. In these difficult times, there is an opportunity for large corporates to step-in and support their smaller suppliers, with their financial strength and higher credit rating. This will be especially pertinent when government support schemes come to an end across the globe, as many suppliers could find that their financial crutch has been removed.” she says.

Another financing tool to consider alongside bank-driven supply chain finance (SCF) is dynamic discounting. Offered by fintech-led third party platforms, dynamic discounting can enable a large buyer to better support its tail end suppliers. This approach has several benefits, says Wallace. “Buyers can use up their excess cash to help their supplier get early payment, and in return, receive a discounted price for the goods/services that they are procuring. This could be particularly attractive in the current negative interest rate environment, given the limited returns available on short-term investments.”

Offering these kinds of financing options could also assist corporate buyers to diversify their supply chains in response to Covid-19, says Eder. “A number of corporates have become aware of the high concentration risk in their supply chains, with over-reliance on a few key suppliers. This has led to delays and holes in supply chains as the crisis has taken its toll. In addition, buyers sourcing from far away locations pre-lockdown are starting to consider regionalising their supply chains, as a way of mitigating the types of supply chain breakages and blockages that we saw at the start of the pandemic. We therefore expect to see large buyers looking to work with a broader base of suppliers going forward, to help ensure resilience,” she explains.

Wallace adds: “Of course, there are logistical considerations to adding new suppliers, especially as the pandemic continues to develop and country-by-country situations evolve. But given that many large buyers could be undertaking the same kind of review of supply chain partners simultaneously, providing a supplier with the option of taking payment earlier than their contractual payment date could prove to be a competitive differentiator for securing a new supplier relationship.”

Driving digital innovation

This focus on financially supporting all levels of the supply chain plays an important role in keeping global trade flowing. But there are additional developments helping to grease the cogs of international trade, not least the push towards increasingly digital trade transactions.

It’s no secret that an archaic over-reliance on paper has long been considered the Achilles heel of trade finance. And due to the cost of implementation and onboarding, alongside regulatory and legal complexities, digital disruption of the trade universe has long seemed like a pipe dream to many. Nevertheless, Covid-19 has prompted a renewed collective push towards the digitisation of international trade finance.

Wallace notes: “At the start of the pandemic, all banks were focused on bringing in ‘workarounds’ to many traditional manual processes and introducing digital solutions in order to maintain the delivery of valued trade finance solutions for clients. I’m delighted that, at Barclays, innovative measures were introduced in mere weeks, bringing significant progress under tight timelines.”

A great example is the adoption of eSignatures in lieu of wet ink signatures for submitting and signing trade finance applications. “Allowing corporates to complete an application form for their international guarantees via DocuSign has enabled us to help keep clients’ trade transactions flowing smoothly during lockdown,” she says. “And as simple as it sounds, enabling virtual signatures for Barclays’ clients across Europe involved close scrutiny of local laws and regulations within each jurisdiction. Cybersecurity was also front of mind, and much work was undertaken behind the scenes to ensure the robustness of eSignatures.”

Another interesting digital development, pioneered by Barclays, has been the amendment of the standard terms of the aircraft leasing sector’s stand-by letters of credit (SBLCs) to allow for electronic presentation of claims in lieu of original hardcopy demand certificates. “This has been particularly useful given the impediments to physical document delivery, including postal delays and even closure of courier services in certain countries,” says Wallace.

Shared progress

As much as digital innovation from individual banks, and in certain industry sectors, has been a huge benefit for corporates during lockdown, it is the wider digital collaboration among industry bodies, trade consortia, and the broader banking community that will be the true silver lining to the Covid crisis. Says Wallace: “In the past, one of the barriers to digitisation has been the alignment of stakeholders. The pandemic has put everyone on the same page: digitisation is no longer a nice-to-have, it is a must-have. Collaboration is accelerating as a result, and practical solutions are emerging in rapid timeframes.”

This is an important point for Eder who notes: “Often, digital projects focus on an ideal – or on using the latest technologies. Yes, it’s good to aim high and to explore the potential of emerging tech, but it’s also important not to overlook existing solutions simply because they aren’t new. There are tweaks that could be made to current products to enable them to be used digitally, as the SBLC example illustrates. Right now, these are the kinds of solutions clients need.”

The same goes in the cash management space, adds Eder. “Corporates hear a lot about application programming interfaces [APIs] being the latest tool for bank connectivity. But building an API ecosystem takes time and investment. Traditional routes like host-to-host could be more appropriate for some companies, and should not be dismissed simply because API connectivity is now considered cutting-edge.”

The key message, Eder stresses, is that it is possible to leverage existing technology to get the basics, such as automation and real-time cash visibility, in place. “The aim is not to achieve this in the most sophisticated way possible, or using technologies that aren’t yet proven. It’s about reaching these goals in the most resilient manner – with a sensible budget and timeframe.” This is even more true when uncertainty around a second wave of the pandemic persists.

“Now may not be the right time to be making investments in bells and whistles. Getting the digital fundamentals right, such as real-time management of cash flows, can deliver immediate benefits. These include working capital optimisation and the ability to better support suppliers – which feed full circle into the SCF developments mentioned earlier. In other words, digitising using existing technologies and solutions in new ways, can actively help to support the recovery.”

Seizing advantages

That’s not to say that looking to future digital developments isn’t also important. Indeed, Barclays is doing just this. Eder continues: “From trade and supply chain finance, to payments and cash management, we are learning from the crisis and innovating around it. We are helping clients not only to work virtually, but also more efficiently. The same goes for our own operations, we are reviewing and amending our workflows and technology investments. We are also proactively teaming up with fintechs and cloud-enabled platforms to bring the best of both worlds to our clients – the trusted and secure bank environment and the flexibility and agility of third-party innovators.

The Covid-19 crisis, says Wallace, has afforded treasurers, banks and fintechs a unique opportunity to change the status quo. “We must continue to move forward, while remaining mindful of the risks we need to protect ourselves and our clients against, such as money laundering, cybercrime and fraud. This means building on the current momentum behind digitisation to continue industry investment in artificial intelligence, machine learning, Distributed Ledger Technology and the Internet of Things – alongside the technologies and financing solutions we all know and trust. To quote Tony Robbins, ‘Change is inevitable, progress is optional.’”