It sure is a hell of a lot easier to just be first.” That’s one of many memorable lines from Margin Call, a 2011 movie about Wall Street. And it’s a good summary of wholesale banking’s stance on AI and its subset machine learning. Corporate and investment banks (CIB) first adopted AI and machine learning decades ago, well before other industries caught on. Trading teams have used machine learning models to derive and predict trading patterns, and they’ve used natural-language processing (NLP) to read tens of thousands of pages of unstructured data in securities filings and corporate actions to figure out where a company might be headed.

Today, some CIB institutions are using AI at scale and reaping enormous benefits. But much of the industry lags behind the leading CIB institutions; many banks are using bespoke, artisan-like approaches that are inherently less productive. Another problem: bankers often see areas across the front, middle, and back offices as too complex to use machine learning. A few leading banks have made AI-related progress on some of these areas, including relationship manager (RM) support and advisory, compliance and risk decisions, and client service on complex bespoke products (think foreign-exchange hedges on forward commodities agreements).

Now comes generative AI: you may have heard of it (ahem). The McKinsey Global Institute (MGI) estimates that across all of banking, wholesale, and retail, gen AI could add between $200 billion and $340 billion in value—for example, through greater productivity. The technology has huge potential for the full CIB business system. As the name suggests, the new tools are incredibly adept at coming up with content that can serve as a first draft in many areas. But they’re also adroit at understanding previously published content; gen AI adds a new element of natural-language understanding (NLU) that can take NLP-based applications to an entirely different level.

Consider a couple of examples. CIB banks can strengthen their compliance work by using gen AI to sort through regulators’ reports, read them intelligently in the way that a junior compliance officer would, find the most relevant report, and then write a synopsis for a senior officer to act on. They can improve their competitiveness in client servicing by using the technology to write documents that are currently produced by hand. And they can tap tools such as Broadridge’s BondGPT to offer investors and traders answers to bond-related questions, insights on real-time liquidity, and more.

Some banks are already starting to capture the opportunity from gen AI. JPMorgan Chase has filed a patent application for a gen AI service that can help investors select equities. Morgan Stanley has built a tool to help RMs deliver relevant ideas to customers in real time. Many other banks, however, are just tinkering at the edges. Still others are hung up on concerns about computing cost or stalled because of intellectual-property constraints.

We firmly believe that banks need to work through their challenges and avail themselves of the significant benefits to be gained from gen AI. In our experience, depending on the application, gen AI can improve productivity in core CIB activities by 30 to 90 percent. All told, productivity and other benefits might add 9 to 15 percent to CIB operating profits, in MGI’s estimate. (We should note that those are the kinds of efficiencies we’re seeing in early use of our own new gen AI tool, Lilli.)

In this article, we look at the areas where gen AI has the most potential for corporate and investment banks, and the risks that banks need to watch for. We conclude with an outline of the capabilities that banks will need if they are to thrive in the era of gen AI.

Where to apply gen AI

Corporate and investment banks are putting gen AI to work across the business system (see sidebar, “Potential applications of gen AI in wholesale banking”). They’re making the most progress in three areas: new product development, customer operations, and marketing and sales.

In new product development, banks are using gen AI to accelerate software delivery using so-called code assistants. These tools can help with code translation (for example, .NET to Java), and bug detection and repair. They can also improve legacy code, rewriting it to make it more readable and testable; they can also document the results. Plenty of financial institutions could benefit. Exchanges and information providers, payments companies, and hedge funds regularly release code; in our experience, these heavy users could cut time to market in half for many code releases.

For many banks that have long been pondering an overhaul of their technology stack, the new speed and productivity afforded by gen AI means the economics have changed. Consider securities services, where low margins have meant that legacy technology has been more neglected than loved; now, tech stack upgrades could be in the cards. Even in critical domains such as clearing systems, gen AI could yield significant reductions in time and rework efforts.

In customer operations, banks are using gen AI to extract, search, and summarise unstructured servicing information and translate it into machine-readable instructions. That comes as a big relief: up to 60 percent of CIB servicing is done through email and manual documentation. In post-trade services, banks are using gen AI to read the documentation on corporate actions—and, critically, banks are using NLU to assess the implications of corporate actions across clients and products. And in the middle office, banks are automating manual tasks. Gen AI is proving capable of writing technical documents such as financial; environmental, social, and governance (ESG); and audit reports. It’s also being used to write loan contracts such as mortgages.

A leading Asian corporate bank, for example, had a problem: its RMs were spending a lot of time painstakingly summarising the bank’s sustainability performance and filling out questionnaires required by each of their B2B clients. To get ahead of the problem, the bank started using gen AI to extract knowledge from across the enterprise to answer the questions that RMs were typically asked. The bank turned these questions into prompts for its large-language model, which was trained on the bank’s ESG-related content. The gen AI tool synthesised material across sources (and named the sources—a must-have), extracted supporting quotes, and stated its confidence in its work. Analysts then took over; they found that the gen AI tool’s answers were 90 percent correct. Now, RMs are saving 90 percent of the time they used to spend on this task.

Marketing and sales is a third domain where gen AI is transforming bankers’ work. The most exciting opportunity might be in relationship management, where gen AI has the potential to take all voice and text interactions with clients (and internal discussions about the client) and use them to create an “RM assistant.” A gen AI–powered tool on the RM’s desktop can help with tasks such as investment ideas, sales, and product policies nearly instantly. This could cut the time needed to respond to clients from hours or days down to seconds. Gen AI can help junior RMs better meet client needs through training simulations and personalised coaching suggestions based on call transcripts.

CIB marketers can also use the new tools to automatically summarise a bank’s knowledge and use it to create viable marketing content, such as market recaps, research reports, and pitch books. A leading investment bank, for example, has built a gen AI tool to help analysts write first drafts of pitch books. The analyst uploads all the relevant documents and then queries the chatbot to ensure it has the material it needs. Then, the analyst can instruct the tool to produce many of the slides that are typically needed and many others that reflect the specifics of the proposed investment. The tool saves analysts about 30 percent of the time they used to spend creating pitchbooks.

These three domains—new product development, customer operations, and marketing and sales—represent the most promising areas for the technology. But other functions can also benefit. Consider loan origination and decisioning. Gen AI can extract textual content from customer interactions, loan and collateral documents, and public news sources to improve credit models and early-warning indicators. Or it can look at risk and compliance support, as many banks are doing, whereby gen AI can provide support to first- and second-line functions to identify relevant regulations and compliance requirements and to help locate relevant instructions. The technology is not yet at a state where banks can have sufficient confidence to hand over risk and compliance tasks fully. But significant contributions are already possible today.

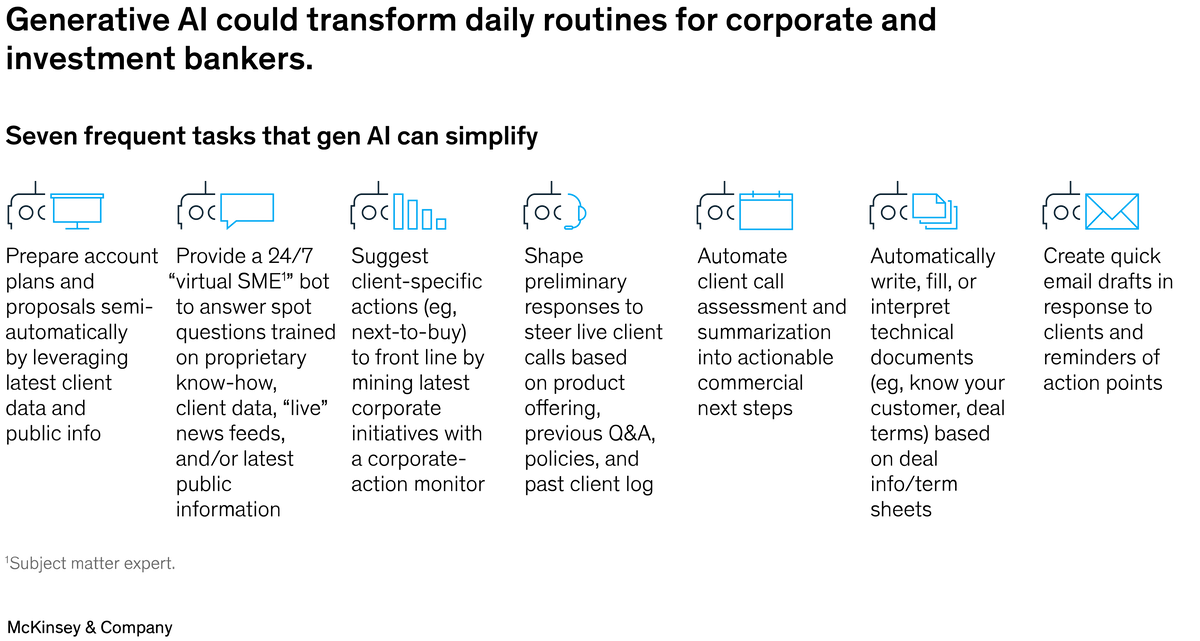

In short, it’s no exaggeration to say that gen AI could transform the day-to-day for wholesale bankers (exhibit).

Ingredients for success at scale

Most CIB institutions are starting with a proof of concept for a gen AI application. To move beyond that stage, banks will want to build on their current capabilities and technology for AI and machine learning to ensure that the following elements are in place:

- A strategic road map. CIB leaders should define a clear strategy of how they want to integrate gen AI into their processes. Does gen AI completely transform their core business (as it might in market- and equity-research support), or does it provide a revenue uplift or productivity opportunity? Early adopters have had good results by starting with a top-down value heat map of the bank’s revenue and cost lines across CIB divisions to locate the potential for value creation.

A consideration of costs must be part of the road map. Every step of developing gen AI—embedding and storing knowledge, supporting thousands of queries daily, building and training new models—can result in significant costs. Banks will need to identify the best combination of models for their intended applications, to not only guarantee accuracy and sustainable performance but also capture the value identified in the road map. - Talent. CIB firms typically have a wealth of AI talent—quants, “strats,” modelers, translators, model explainers, and so on. This raises some questions: Can these employees add gen AI to their skill set? Or will the firm require new capabilities? And how should banks organise these experts for gen AI? Market leaders are establishing cross-functional teams across product segments and IT businesses in line with previously tested and highly successful AI delivery models. Another issue we’ve seen crop up: new users will need to know how to use the gen AI tools they’ve been given. How can banks build so-called prompt-engineering academies at scale?

- Data. Most CIB firms are already working to consolidate and optimise market, reference, and client data. But they don’t always have a strategy for unstructured data such as text, images, client documents, and so on. All of these can be vital for successful gen AI applications; firms may need to establish the infrastructure for people across the firm to access unstructured data from anywhere on their platforms.

- Technology. Unlocking value from gen AI will require a lot more than a subscription to a chatbot service. Leaders are finding that to fully capture productivity gains throughout a process, they need modern infrastructure and a clean architecture and systems landscape that is able to consume and receive AI-created instructions (such as platform-wide workflow tooling and APIs). These firms are also opting for a hybrid infrastructure approach, such that they can work with private models for sensitive data and still explore the public-cloud capabilities that are progressing day by day.

Risks to watch out for

Organisations will need to be mindful of and carefully plan for risks associated with scaling generative AI. Here are some of the major concerns that CIB firms will need to address:

- Impaired fairness. Gen AI may project algorithmic bias because of imperfect training data or engineering decisions in both the development and deployment phases.

- Privacy concerns. Gen AI may heighten privacy concerns through unintended use of client-sensitive information in model training, thus generating potentially sensitive outcomes.

- Security threats. New applications may be subject to security vulnerabilities and manipulation (for example, users or bad actors may bypass safety filters through obfuscation, payload splitting, and virtualisation).

- ESG impact. Training and deployment of foundation models may increase carbon emissions, thus exceeding commitments or expectations. And gen AI may disrupt or in some cases displace workers, introducing reputational risk and potential talent shortages.

- Computing cost. At-scale use of gen AI will require either using dedicated hardware or significantly increasing cloud workloads. Should that happen, cloud providers will naturally seek compensation, even if they effectively subsidise gen AI experiments at the moment.

In short, gen AI models create a new set of risks that will need to be managed. As they build new gen AI models, banks will also have to redesign their model risk governance frameworks and design a new set of controls.

Over the past ten years or so, a handful of corporate and investment banks have developed a genuine competitive edge through judicious use of traditional AI. Now, the race is on to do so again with an even more transformative technology.

This article was originally published by McKinsey & Company, www.mckinsey.com. Copyright (c) 2023 All rights reserved. Reprinted by permission.