Treasury Strategy & Transformation

After the Ballots

How the ‘year of elections’ reshaped treasury priorities

Published: March 21, 2000

Efficient, timely collections are a priority in every industry, and each has a different set of challenges according to collection volumes, customer base and business organisation. Like other industries, the United States insurance sector has experienced a large number of mergers and acquisitions in recent years, which can result in fragmentation of business processes. Moreover, with a large numbers of both retail and institutional customers and a very high volume of collections, the insurance sector in the United States is going through a period of significant change as electronic payment methods replace checks, and insurance firms seek new ways of ensuring process efficiency to increase their competitive advantage.

To understand some of the needs, challenges and opportunities in treasury collections amongst insurance companies more fully, BNY Mellon commissioned a research project with an independent consultancy firm, involving some of the leading insurance companies in the United States. This project revealed significant insights into the insurance segment, but many of these can also be applied to other business segments. This article highlights some of the key findings of this project.

Centralization of financial processes, including collections, has become a key theme for all industries as companies seek to maximize efficiency of processes and visibility of information. The project revealed that although ‘centralization’ is a commonly used term, it is often interpreted differently, referring variously to use of common systems/processes for collections in multiple locations, centralization of processes by business line/subsidiary, or centralization of collections into a single location based on a single technical infrastructure. Although many firms describe their collections process as ‘centralized,’ in most cases this referred to centralization by business line, with each segment organizing its collections activities independently, as opposed to having a cohesive set of collections processes in a single location.[[[PAGE]]]

A segmented approach to collections creates a variety of challenges, not least the difficulty in collating data held in different parts of the business, which makes it difficult to implement best practices and management reporting in a consistent way, and to establish consistent and meaningful key performance indicators (KPIs). In the insurance industry, these issues are more acute due to the frequency of M&A activity.

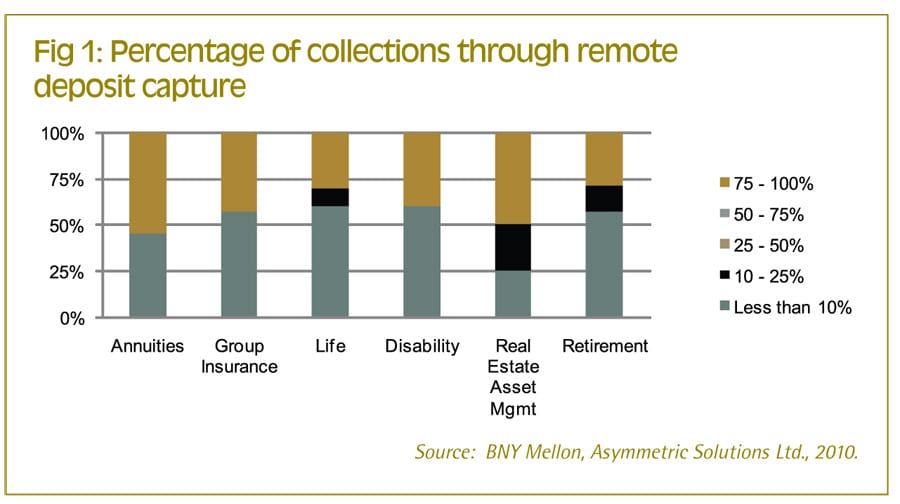

There are increasingly techniques available to automate collections processing, such as remote deposit capture (RDC). Such techniques have been introduced by the majority of insurance firms, across most business lines, but there are considerable differences in the degree of adoption, with either a small minority or large majority of collections processed in this way (fig 1). These variations across firms suggest that for some organizations, there are still considerable efficiencies that can be gained using tools already in place.

There is a universal drive for increasing the proportion of payments that is collected through electronic methods such as ACH and ACH Debits. Firms have so far had mixed success in achieving this, primarily due to differences in business organization, M&A activity and the length of time for which this has been a priority. Linked to this, the issue of whether, and how, to accept card payments without eroding margins is a growing issue with competitive implications. Some firms have introduced card collections already, although in a limited way so far, yet this potentially creates competitive advantage amongst customers wishing to use debit or credit cards to pay insurance premiums.

“One of our challenges is working out how to deal with the increasing demands on the insurance industry to accept credit cards. Some are already starting to do so, which adds to the pressure on others. Clearly, credit cards are an expensive way of collecting premiums, which therefore erodes margins; furthermore, it is not a legal form of payment for some business lines. This makes it difficult to implement rules that are easy to implement by our agents, and the onus is on them to make the right decisions with regards to customer payments. Consequently, we, like others, are reticent to move into card payments at present.”

Vice President, Treasury, US Insurance Firm[[[PAGE]]]

Collections technology is often fragmented across the business, particularly as a result of M&A, potentially leading to higher administrative costs, difficulties in integrating systems with bank workstations and other internal systems, and a loss of data integrity when transferring data between systems. Although firms are often seeking to rationalize their systems infrastructure, this will require cohesion across the business, which may be difficult without centralized decision-making over the collections function. The insurance sector typically relies on proprietary (in-house developed) technology for collections, which often leads to difficulties in integrating new opportunities for efficiency and regulatory requirements.

Mail float is not considered a major issue for insurance firms that are cash rich, particularly in a low interest rate environment, and indeed, many respondents did not measure average mail float. However, particularly as economic conditions change, there are potentially working capital, investment and cash flow forecasting advantages in monitoring and minimizing mail float.

“Mail float is not a key driver in our collections process. In our Life business, we collect from across the United States into one lockbox, so we are fairly neutral about mail float. What we do not know is whether this is the ideal solution, or whether we would benefit from multiple lockboxes. In our current arrangement, although we may lose time waiting for checks to be received into the lockbox, there are gains in terms of back-office processing. We may reconsider this with the growth of imaging; in the short term, in a low interest rate environment, mail float is less of an issue. However, we try not to make major changes too often to avoid disruption to our customers.”

Assistant Treasurer, US Insurance Firm

The challenge of unreconciled collections and late payments is less of an issue for the insurance industry than other business segments, as policy numbers can be used for reconciliation, and policies lapse in the case of significantly late payment. However, timely reconciliation remains important in terms of customer service, working capital management, investment and forecasting to ensure that processes for prompt reconciliation and collection are efficient and accurate.

Although bank relationships are maintained by treasury in many cases, business segments often have different perceptions about their banks. By understanding each business line’s requirements and priorities from their banking relationships, treasury can help improve the experience of business unit users, often in quite simple ways, such as reformatting reports. Bank relationship is the most important priority for most business lines, followed by customer service. This illustrates that banking is a service industry, and although banking products are important, particularly for certain business lines, the relationship and support received from banks is critical to a successful partnership.[[[PAGE]]]

Bank technology, as the means of providing timely, accurate information, is an important issue for insurance companies as it is for other industry sectors.

“What we need from our banks is a combination of the right information and the right tools for interacting with the bank. From an information reporting standpoint, we need data to be made available in a variety of different formats for integration with various systems. We also need tools to interact with the flow of data in the lockbox real-time.

Assistant Treasurer, US Insurance Firm

Insurance firms have high collection volumes, so it is surprising that relatively few have yet implemented SWIFT connectivity with their banks, although these companies typically maintain relatively few banking relationships, due to the potential efficiency and bank independence that can be achieved. However, this is starting to change as some early adopter firms implement SWIFT:

“We have now gone live on our first four banks on SWIFT, initially for external payments through our treasury management system, but we are adopting a phased approach, layering in more functionality over time, and intend to communicate with all of our banking partners through SWIFT.”

Group Treasurer, US Insurance Firm

Improvements to internal technology and integration is the most important priority for most firms, irrespective of business line, which includes a variety of different project types, including eBilling, remote deposit capture, integration with banking systems, overall systems maintenance and upgrades. Dealing with electronic payment methods, including the dilemma of accepting card payments is an important short-term priority.

Business process improvement and increased centralization are also important, but generally these are medium/long-term priorities.

There has been little exploration of trends and challenges for treasurers in the insurance industry, and it has been interesting to note the degree to which respondents revised their future priorities based on their participation in the study. Collections are a challenge for every industry, as companies seek to accelerate the cash flow cycle, minimize credit risk and maximize working capital. The insurance sector is experiencing a number of challenges; in particular, the need to centralize and increase efficiency and visibility over collections, while leveraging electronic payment methods. With a very high number of retail customers, the challenge will be to encourage conversion to efficient, electronic payment methods such as ACH and ACH Debits, whilst finding ways of accepting credit and debit card payments in a cost-effective way. Over the coming year, we would expect to see mail float, bank connectivity, remote deposit capture and centralization of processes become more significant issues. Those firms that take advantage of new opportunities in these areas have the potential to create competitive advantage, reduce costs and increase margins.

How the ‘year of elections’ reshaped treasury priorities

The recent EACT Summit underscored treasury’s contribution in the face of adversity.

Infosys and BNP Paribas collaborate on a scalable global receivables purchasing facility.