- Eleanor Hill

- Editorial Consultant, Treasury Management International (TMI)

5 Practical Steps for Preparing Ahead

No-one knows precisely what the future holds, but a successful digital treasury team must be able to adjust quickly to the evolving ecosystem – and be able to scale at speed. In this article, four industry experts outline their visions of a digital treasury function in 2030 and explain how to start laying the foundations for these future goals, today. They touch on everything from embedded finance to best-of-breed architectures and innovative ways to offset carbon emissions through treasury products.

“For tomorrow belongs to those who prepare for it today.” Over the years, this African proverb has been transformed into pithy quotes from world leaders and changemakers – and its relevance still rings true, especially in the business world.

Of course, there will always be unpredictable factors treasury teams cannot prepare for. Before 2020, few had predicted a world of global lockdowns and remote-working due to a Coronavirus pandemic. Nevertheless, there are many elements of the future that treasury leaders can start preparing for today:

1. Embrace total automation of day-to-day processes

“Automation is a treasury trend that’s been talked about for several years now – because teams spend so much of their time on low value tasks and the management of manual processes. In 2021, we have already seen a number of leading treasury teams looking to embrace technologies such as robotic process automation (RPA) and artificial intelligence (AI) in order to reduce their manual burden, with the aim of only dealing with exceptions,” says Conor Maher, Head of Transaction Banking Products, NatWest. In fact, 16% of treasurers surveyed by TMI and NatWest in Q2 2021 stated that implementing AI is currently their number one digital priority.

Conor Maher

Head of Transaction Banking Products, NatWest

Nevertheless, a significant proportion of treasury functions are still highly manual – with spreadsheets still surprisingly common, even in large corporates. Nick Pedersen, Global Head of Digital, NatWest Markets confirms this, stating: “Many companies still use Excel for their FX reporting, even if they have sophisticated ERP, TMS and portal set-ups for the rest of their treasury needs.”

Ideally, by 2030, Pedersen would like to see the treasurer as the “designer of the FX policy, but with no involvement in its execution”, since this would be performed automatically, through an end-to-end journey. “This means that when an exposure of a cash-flow arrives at one part of the organisation an FX trade or a hedge is executed in real-time,” he says. “Some of the companies that we work with in the tech sector are fairly close to having this in place today, but as a wider concept, it will take time for other sectors to catch up,” he believes.

Maher echoes Pedersen’s goals, adding that: “Total automation of the treasury function – from cash management to FX risk management and beyond is the nirvana for 2030. Achieving this goal, or coming as close to it as possible, will free up treasury teams to concentrate on value adding activities such as horizon scanning and formulating new company strategies.” At present, the treasurer spends a great deal of time looking in the rear-view mirror, explains Maher, but automation can empower them to look into the future and get ahead of emerging trends.

Under the skin of tech acronyms

To find out more about garnering the benefits of APIs, AI, RPA and a host of other digital treasury technologies, download our No-Nonsense Guide to Digital Treasury: https://admin.treasury-management.com/articles/taking-digital-treasury-to-the-next-level-a-no-nonsense-guide/

“This will be critical in the real-time environment of 2030, where end of day processing no longer exists,” comments Maher. By then, almost all payments will likely be moving instantly across borders, as real-time schemes come to fruition, SWIFT gpi gathers pace and Central Bank Digital Currencies (CBDCs) potentially come into their own.

Matthew Giannotti, Head of Transaction Services Sales FI & Professional Services, NatWest, adds: “By 2030, corporates will have to adapt to the 24/7 way of life. They will need the ability to make decisions based on intra-day information. So, either treasury needs global teams who can keep a 24/7 eye on the financial markets and the company’s cash positions and risk exposures, or they need an automated AI-based tool that can do that for them, and send alerts when action is needed.

Making change happen:

To achieve this level of ‘total automation’, treasurers’ attention will undoubtedly turn to systems set-ups and the availability of third-party solutions. “After defining their goals and digital treasury vision, the next step is to understand and measure the capability of the treasury team – and assess the need to partner or outsource – in meeting those automation aims.”

Also important is the assessment of the existing treasury infrastructure in terms of delivering, managing, processing, and analysing real-time data. With the support of their chosen partner(s) or own IT team, treasury will more than likely need to look at the implementation, or augmentation, of technologies including:

Of course, the flipside of automation is the impact on human capital. And this must be carefully considered as part of any 2030 plan.

Matthew Giannotti

Head of Transaction Services Sales FI & Professional Services, NatWest

2. Embed open banking as standard

Within the next decade, open banking should have matured to the point where it is embedded within the treasury psyche. Austin notes: “In terms of treasury advantages, open banking already offers the potential for multi-bank cash, trade and FX visibility at the touch of a button – which dovetails nicely with the vision of a fully automated treasury function. It is also making waves in the payments space.”

Elsewhere, open banking also paves the way for other, more existential changes within organisations – and this is where the concept will likely mature most by 2030. The rise of embedded finance (see point 4) is one such trend, while open infrastructures are also shaking up traditional ways of organising processes and systems (see point 3). As such, there are strategic conversations that can be taking place today within finance departments and boardrooms that could lay the foundations for a new, open, approach in the years ahead.

Making change happen:

“Corporates wanting to make progress on open banking should challenge their banking partners to introduce relevant solutions sooner rather than later,” says Maher. A few leading banks have rapidly taken up the open banking mantle for corporates, but many have concentrated solely on the consumer side. Giannotti continues: “It’s time for cash management providers to start moving more swiftly on the corporate benefits of open banking. At NatWest, we have seen this as an opportunity from day one – investing in services such as Payit™, for example.

‘We’re excited by the possibilities that open banking holds and certainly want to be at the forefront of innovation here. But we also rely on our corporate clients to challenge us to solve their true pain points. Through that dialogue, we can create real-world solutions based on open banking that will carry treasury through to 2030 and beyond.”

All about open banking

For those who have been too busy to give it much attention, open banking is an infrastructure that facilitates the secure sharing of financial information as well as payment instructions – through the use of open APIs. It is quickly becoming a global phenomenon, although the UK is arguably leading the way at present.

In the treasury space, a handful of solutions already exist which leverage open banking rails to provide corporates new ways to send and receive online payments. Payit™ by NatWest is a great example and the benefits include the ability to easily reach non-NatWest customers, no requirement to hold customer data, real-time transactions, and a reduced potential for fraud.

To refresh your memory on the origins of open banking, and the benefits for treasury, our recent article Open Your Eyes to the Benefits of Open Banking. https://admin.treasury-management.com/articles/open-your-eyes-to-the-benefits-of-open-banking/

3. Consider a best-of-breed tech ecosystem and fintech partners

With the capabilities of APIs clear for all to see and the evolution towards an open, collaborative financial ecosystem, we may also see more of a best-of-breed approach to technology selection in 2030, believes Giannotti. “Rather than having a single ERP or TMS, treasurers might build their own dashboards, using APIs to plug in the information they need and want – direct from different sources, such as banks, fintechs, trading platforms and market information providers,” he explains.

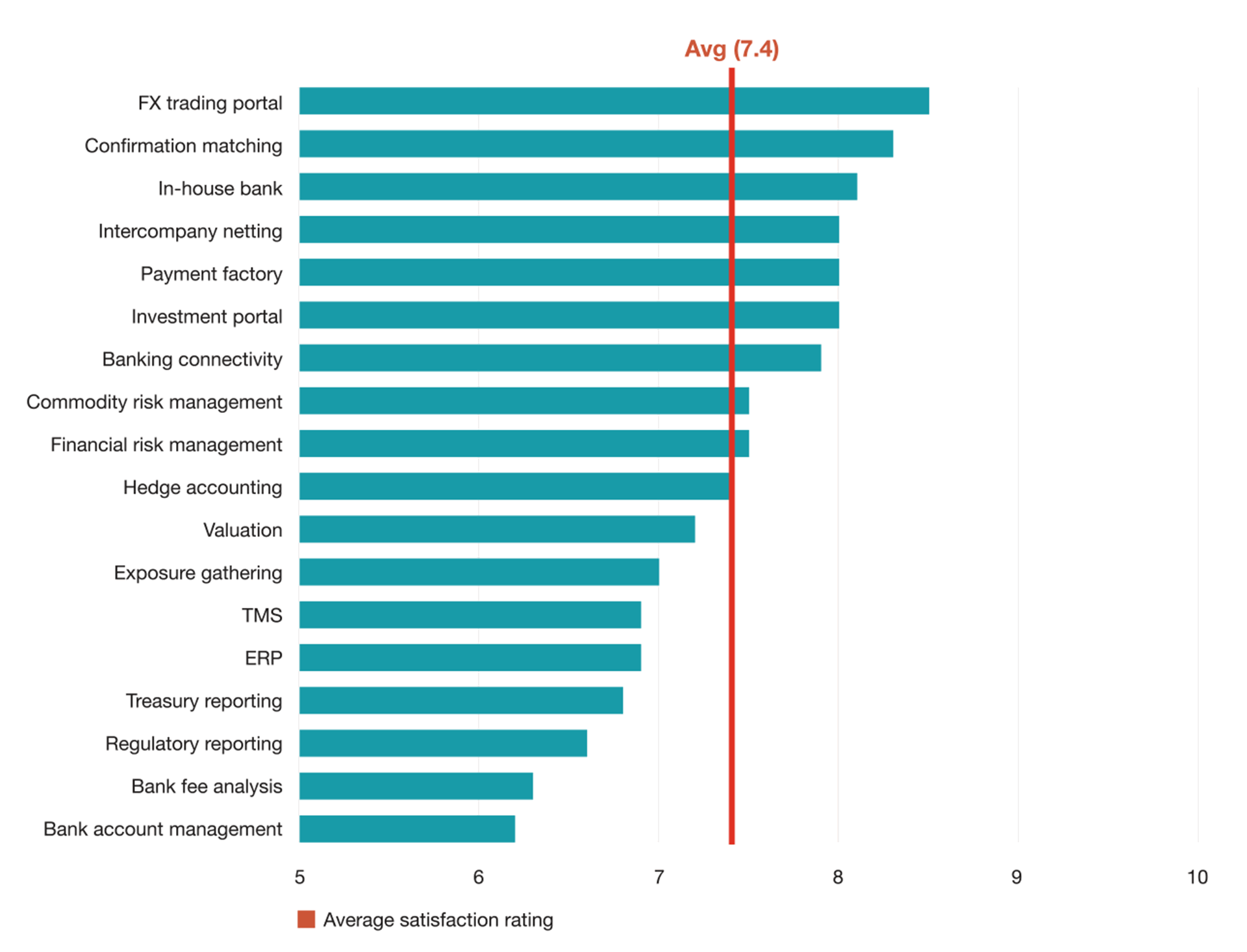

This approach enables the use of multiple specialised systems, which of course, can provide organisations with specialised features – and may prove more satisfactory than an all-in-one solution such as an ERP or TMS (see Fig. 1). Through a best-of-breed set-up, treasury can access the cream of solutions and providers in the market, in a manner that suits them. Pedersen adds: “This is not necessarily a new concept for treasury but newer technologies are making it easier to achieve. And it would be great to see FX systems no longer being out on a limb, but part of a complete treasury tech ecosystem.”

Fig 1 Niche systems achieve higher satisfaction rates than all-in-one treasury systems

Source: PwC 2019 Treasury Benchmarking Study https://www.pwc.co.uk/audit-assurance/assets/pdf/global-corporate-treasury-benchmarking-survey-2019.pdf

Making change happen:

Challenging banks and tech providers will be critical to making best-of-breed a reality by 2030. Working with fintechs may also need to become a more mainstream activity for treasurers and banks alike.

Giannotti comments: “A handful of corporates who we work with are already very comfortable with fintechs – and work with them via bank partnerships or directly. I expect this trend to accelerate significantly as we head towards 2030.” Pedersen agrees, adding: “By then, fintechs will be much more established and have the track record to prove to treasurers that they are in this for the long haul – and that they are prepared to work with incumbents and plug in to legacy systems to suit the needs of the treasurer, rather than being entirely disruptive.”

While this 2030 vision sounds beneficial from a treasurer’s perspective, there are clear hurdles to overcome, cautions Maher. “Best-of-breed currently exists in a microcosm. By 2030, treasurers operating this model will be dealing with multiple contracts with vendors and fintechs, which could cause complexity in terms of responsibility if any issues arise.” Austin adds: “Treasurers also need to be extremely careful who they work with. The fintech space is still crowded. Trust is paramount.”

Rowan Austin

Head of Trade Origination and Advisory, NatWest

4. Leverage Banking-as-a-Service

APIs, open banking and fintechs are also fuelling the emergence of ‘embedded finance’ – or ‘banking-as-a-service’ (BaaS) – a trend that is expected to change market structures and business models over the coming decade [2]. Maher explains: “In simple terms, this is when a financial service, like payments or insurance, is embedded into a non-financial brand as a means to create a seamless customer experience.”

Certain transport and food delivery firms already offer this kind of service within their apps – but this trend is expected to grow enormously by 2030. In fact, by that date, the market for embedded finance is anticipated to be worth $7 tr.[3]. Maher continues: “Embedded finance is not necessarily directly within the treasurer’s remit, but it will touch and influence their areas of responsibility, and we see it as a key trend shaping the future environment.”

Making change happen:

The onus around making BaaS a reality by 2030 lies on the banking and fintech side. Nevertheless, says Maher, “Treasurers in consumer-facing sectors may wish to engage early with their banking partners around this industry shift. There are also strategic conversations to be had with the board around the value of a seamless digital customer journey in terms of making cash flows more predictable and visible.”

5. Push the boundaries of ESG

As we head into the next decade, and board level focus on ESG continues to intensify, Pedersen expects to see much more solution innovation in this area, across product lines. “It is our role as banks, to rapidly adapt to meet corporate’s evolving ESG needs,” he states.

Austin agrees, adding that “Managing supply chains used to be about drilling costs down as low as possible. Now it’s about overlaying ESG and resilience, to create a supply chain that is sustainable in every possible sense of the word.” While banks have been innovating heavily in the ESG space of late, with green and sustainable - loans, bonds, deposits, supply chain finance and more – “there is always room for additional experimentation as we head towards 2030,” says Maher.

Nick Pedersen

Global Head of Digital, NatWest Markets

Making change happen:

While there are ESG projects treasury teams can take on internally, such as reducing team paper consumption and choosing banking partners with excellent sustainability credentials, the bulk of innovation will happen in the products space.

Pedersen comments: “Again, this is an area where treasurers can look to push their banking partners to be more creative and to overcome perceived hurdles. When we were working on the solution with Drax there were challenges to overcome before we could get the product to market – but we made changes to the traditional ways of working, and it paid off.” Regulators may also need to be lobbied, says Austin, who sees the lack of standardisation in the sustainability space” as a hurdle to rapid progress.

Maher adds: “2030 is a landmark year that many climate goals are being aligned to. Corporate treasurers can no longer afford to think that ESG is someone else’s responsibility – nor can their relationship banks. Together, there is a possibility to work towards solutions that can have a positive impact in the real world. Co-creation is the watchword.”

Cutting-edge ESG innovation at Drax

One great example of such innovation is ESG-linked FX derivatives, which have just been launched by NatWest. Thanks to the solution, UK-based Power Generator, Drax, is now applying its long-term ESG key performance indicators (KPIs) to short-term FX trades – including forwards, swaps and options – executed through NatWest and another partner bank.

In practice, Drax’s ESG-linked agreements aim to incentivise reduction in carbon intensity on an annual reducing target that is designed to become more challenging if the company constantly over-delivers. That metric is validated annually against information published in its annual report and accounts and independently reviewed for accuracy and reliability beforehand.

Find out more about this project in issue 281 of TMI: https://admin.treasury-management.com/articles/drax-highlights-core-sustainability-credentials-with-novel-esg-linked-fx-solution/

Nine-year countdown

With so much change set to happen, being surrounded by the right support system will be critical – including a switched on treasury team. Pedersen calls for “innovation to be baked into the treasury team’s culture.” While Maher says that, “Having a team that is dynamic and open to change will enable the organisation to flex relatively quickly, to unexpected threats as well as to opportunities such as those outlined above.”

But Giannotti cautions that: “The technology transition as we head towards 2030 is in many ways easier than the people changes that will be required.” There are social changes that go hand-in-hand with technological ones, he notes. “Some team members may be resistant to change due to fear of job cuts. Others may need training on new technologies, as well as the cyber risks that come with the digital environment, in order to enable them to perform at their best.”

The good news is that treasurers, and their banking partners, have nine years until the 2030 milestone is reached. But this is not the time for kicking the can down the road – preparation is needed to be ready for this new environment. Continuous investment and development are essential. And as Austin concludes, “The time for transformation is now.”