Head of International Fixed Income, Northern Trust Asset Management

Exclusive insight for TMI subscribers! Northern Trust Asset Management share a monthly market commentary for treasurers.

Eurozone Market Update

In May, the ECB raised its three key rates by 25 bps, taking the deposit rate to 3.25%, in line with our expectations and those of the market. This ended the jumbo hikes we had seen since the end of 2022. The ECB's statement was more balanced, maintaining the ”data dependency” language for future decisions. However, it added focus on the transmission of policy, noting ”lags and strength of transmission to the real economy remain uncertain.” Speaking about the previous month’s banking turmoil, ECB President Christine Lagarde stated that European banks still looked resilient but struck a hawkish tone by noting that the ECB had more ground to cover, given the upside risk to inflation.

Euro Short Term Rates

Source: Bloomberg, data as at 31 May 2023

UK Market Update

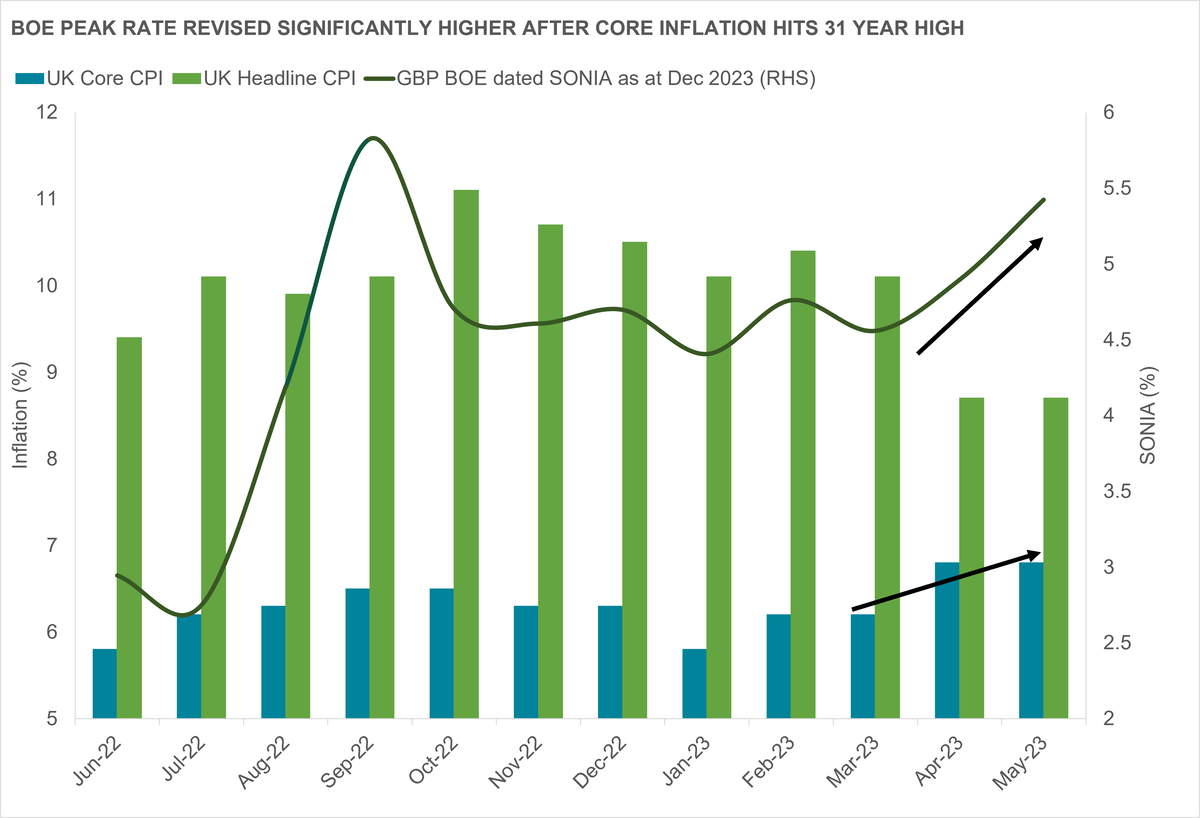

As widely forecasted, the BoE again increased its policy rate by 25 bps to 4.50% in May. The vote split remained unchanged from March at 7-2. Gross domestic product forecasts were revised higher, and there was an indication that any spillover from global banking sector turmoil would have little impact on the UK economy. The main shock came from inflation — while annual headline inflation in April dropped to 8.7% from 10.1%, this was well above market and BoE expectations. More significantly, annual core inflation accelerated to 6.8%, a 31-year high and notably higher than March’s 6.2% reading (see Chart of the Month). Swiftly after the shock, the markets immediately priced in a 25 bps hike for June, with some talk of the terminal UK rate priced in at 5.5% by Q4 2023.

GBP Short Term Rates

Source: Bloomberg, data as at 31 May 2023

US Market Update

After much political tension and some worries over a potential US government default, Congress approved a suspension of the debt ceiling to January 2025 and President Joe Biden signed it into law. Earlier in May, the Federal Open Market Committee raised its target range for the federal funds rate by 25 bps. The policy statement removed language indicating that additional tightening “may be appropriate.” Instead, the committee noted that “…determining the extent to which additional policy firming may be appropriate…” will be highly data-dependent. Chair Jerome Powell reiterated the committee’s view that inflation would come down, but not as quickly as they would like to see, and that rate cuts would not be appropriate if the committee’s view of the inflation outlook proves accurate.

USD Short Term Rates

Source: Bloomberg, data as at 31 May 2023

Looking Ahead

After making 25 bps hikes in May, the Fed, ECB and BoE return for further monetary policy meetings in June. Inflationary pressures remain elevated across all three markets, with core prices remaining sticky. This continues to create a problematic environment for central banks to take their foot off the pedal for now. These pressures are more pronounced in the UK with the strong UK inflation. Governor Andrew Bailey emphasised the evidence will guide decision-making, so we will continue to pay particular attention to the incoming data across all three markets to determine the future path of policy rates. We remain committed to our view that market expectations of policy easing are premature as core price pressures will keep central bank policy rates elevated for an extended period.

Chart of the Month: UK core inflation spike highlights the challenge still facing BoE

Source: Bloomberg, data as at 31 May 2023

For Europe and Asia-Pacific markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Northern Trust and its affiliates may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Opinions and forecasts discussed are those of the author, do not necessarily reflect the views of Northern Trust and are subject to change without notice.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

Forward-looking statements and assumptions are Northern Trust’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

The Northern Trust Company of Hong Kong Limited (TNTCHK) is regulated by the Hong Kong Securities and Futures Commission. In Australia, TNTCHK is exempt from the requirement to hold an Australian Financial Services Licence under the Corporations Act. TNTCHK is authorized and regulated by the SFC under Hong Kong laws, which differ from Australian laws. In Singapore, The Northern Trust Company of Hong Kong Limited (TNTCHK), Northern Trust Global Investments Limited (NTGIL), and Northern Trust Investments, Inc. are exempt from the requirement to hold a Financial Adviser’s Licence under the Financial Advisers Act and a Capital Markets Services Licence under the Securities and Futures Act with respect to the provision of certain financial advisory services and fund management activities.