- Daniel Farrell

- Head of International Fixed Income, Northern Trust Asset Management

Exclusive insight for TMI subscribers! Northern Trust Asset Management share a monthly market commentary for treasurers.

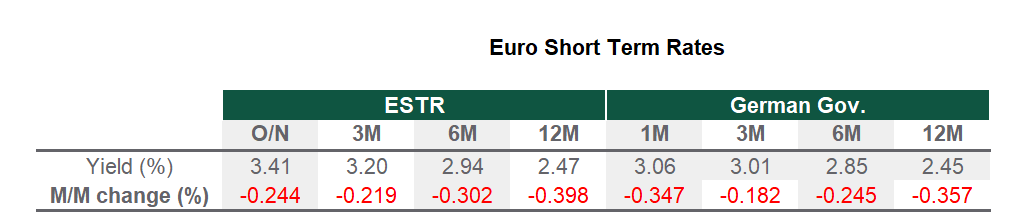

Eurozone Market Update

In September, the ECB cut its deposit rate by 25 bps to 3.5%. It also narrowed the spread as planned between the main refinancing operation and deposit rate facility from 50 bps to 15 bps to limit market volatility without causing significant disruption to money market activity. Eurosystem staff projections for headline inflation remained steady, but core inflation was revised up by 0.1% for 2024 and 2025, and growth forecasts were revised down by 0.1%. ECB President Christine Lagarde pledged not to pre-commit to a particular rate path and again emphasised a data-driven approach. We expect the ECB to continue easing quarterly, with another 25 bps cut likely in December. Services inflation remained sticky in August at 3.5%, up 1.8 percentage points, but that does not move the needle for a cut in October. However, September’s flash Purchasing Managers’ Index (PMI) data and Euro Area Inflation data did bring a lot of sentiment for an October cut, painting a weak growth picture with a loosening labour market. The composite PMI for the euro area fell by 2.1 to 48.9, signalling contraction and delivering the lowest level since February.

Source: Bloomberg, data as of 30 September 2024

UK Market Update

The BoE Monetary Policy Committee (MPC) voted 8-1 to keep the bank rate at 5.00% in September. The vote split gave the meeting a slightly hawkish tilt as most expected two votes for a 25 bps cut. We had expected no cut, anticipating the MPC will reduce rates on a quarterly frequency in 2024 until reaching the neutral point of 3.50% in 2025. The MPC highlighted uncertainties around wage-driven services inflation, rate restrictiveness, fiscal risks and the upcoming autumn budget. While services inflation is expected to ease, headline inflation may rise. In our view, the most important sentence in the statement was: “In the absence of material developments, a gradual approach to removing policy restraint remains appropriate”. This supports our view that the MPC will proceed carefully. Markets fully price in a 25 bps cut in November, with the risks tilted to an additional cut in December.

Source: Bloomberg, data as of 30 September 2024

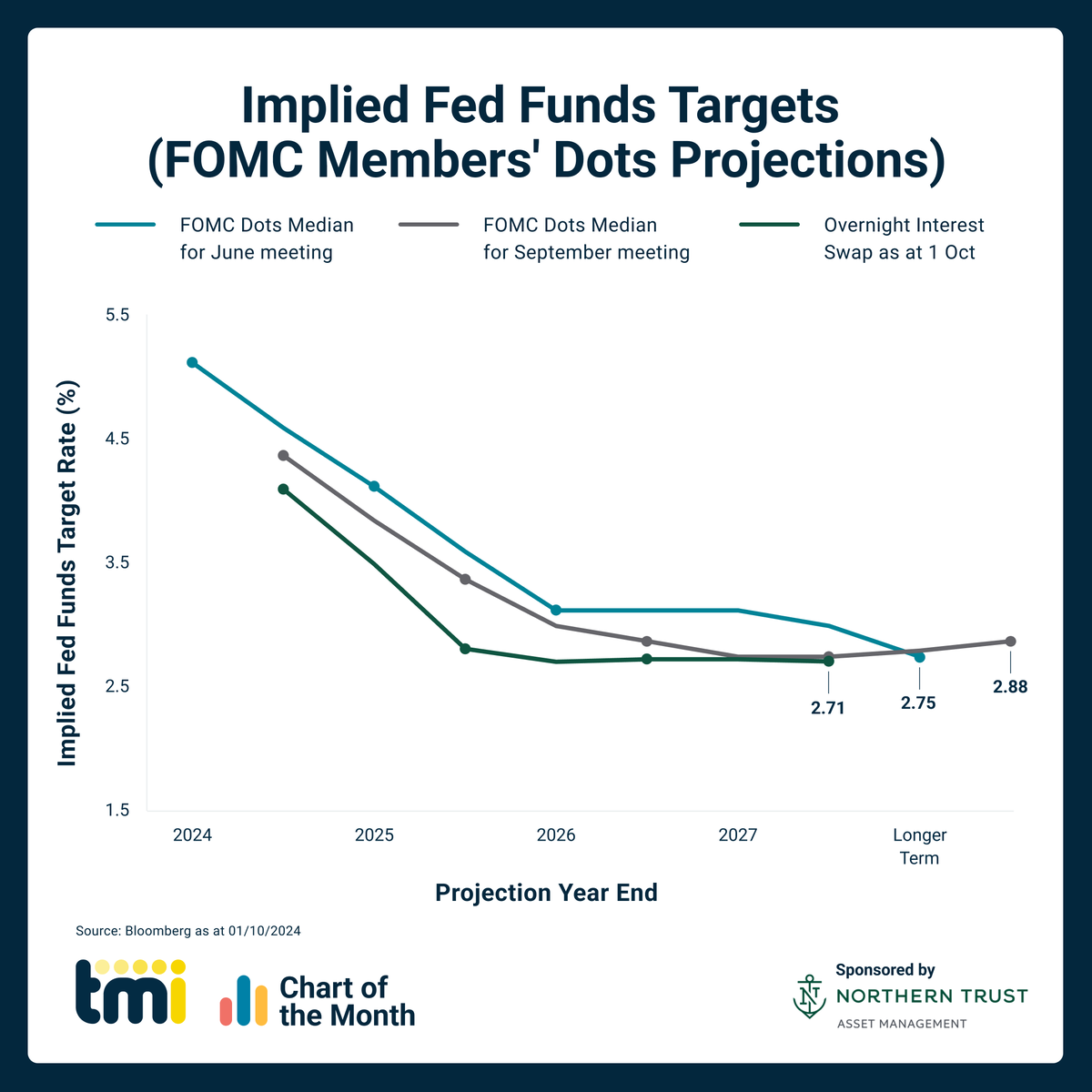

US Market Update

In September, the Fed cut rates by 50 bps amid market debate over whether the cut would be 25 or 50 bps. While the decision to cut was unanimous, Governor Michelle Bowman favoured a 25 bps cut, marking the first dissenting voice since 2005. The FOMC statement emphasised commitment to “support maximum employment and return inflation to its 2% target”, with employment a new addition to the statement. Chair Jerome Powell clarified that the decision doesn't pre-commit future cuts. The latest Summary of Economic Projections (SEP) showed participants expect the federal funds rate to end 2024 at 4.4%, down from 5.1% in June’s SEP. The dot plot (see Chart of the Month) of FOMC members’ thoughts on future interest rates showed nine members favoured 50 bps cuts this year, nine preferred 25 bps and one saw more than 50 bps of cuts in the rest of 2024.

Source: Bloomberg, data as of 30 September 2024

Looking Ahead

In September, the Fed joined other developed market central banks in shifting toward easier monetary policy. However, despite this alignment, each bank faces distinct growth and inflation challenges, setting them on diverging paths. The Fed’s approach will hinge on the balance between its dual mandate — full employment and stable inflation — and we remain cautious about market expectations for aggressive rate cuts. The BoE’s signal for a gradual pace of easing supports our view of quarterly cuts, aligning with Chief Economist Huw Pill’s “Table Mountain” analogy. Meanwhile, ECB President Lagarde has stressed that the bank is not data-point-dependent. Given the limited data available before the ECB’s October policy meeting, we believe the probability of remaining on hold is greater than that of a cut, but we acknowledge the risks are tilted to a faster pace of policy normalisation. Heading into 2025, views among the ECB will become more diverse, given continued downward pressure on growth but slow signs of disinflation in services. With the downside risk to the growth outlook, we expect some members will vote for consecutive cuts, which we believe would be warranted, ending the cutting cycle in 2025.

Chart of the Month

Source: Bloomberg as of 1 October 2024

IMPORTANT INFORMATION

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors.

The information contained herein is intended for use with current or prospective clients of Northern Trust Investments, Inc (NTI) or its affiliates. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Northern Trust Asset Management’s (NTAM) and its affiliates may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For additional information on fees, please refer to Part 2A of the Form ADV or consult an NTI representative.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Hypothetical portfolio information provided does not represent results of an actual investment portfolio but reflects representative historical performance of the strategies, funds or accounts listed herein, which were selected with the benefit of hindsight. Hypothetical performance results do not reflect actual trading. No representation is being made that any portfolio will achieve a performance record similar to that shown. A hypothetical investment does not necessarily take into account the fees, risks, economic or market factors/conditions an investor might experience in actual trading. Hypothetical results may have under- or over-compensation for the impact, if any, of certain market factors such as lack of liquidity, economic or market factors/conditions. The investment returns of other clients may differ materially from the portfolio portrayed. There are numerous other factors related to the markets in general or to the implementation of any specific program that cannot be fully accounted for in the preparation of hypothetical performance results. The information is confidential and may not be duplicated in any form or disseminated without the prior consent of NTAM.

This information is intended for purposes of NTI and/or its affiliates marketing as providers of the products and services described herein and not to provide any fiduciary investment advice within the meaning of Section 3(21) of the Employee Retirement Income Security Act of 1974, as amended (ERISA). NTI and/or its affiliates are not undertaking to provide impartial investment advice or give advice in a fiduciary capacity to the recipient of these materials, which are for marketing purposes and are not intended to serve as a primary basis for investment decisions. NTI and its affiliates receive fees and other compensation in connection with the products and services described herein as well as for custody, fund administration, transfer agent, investment operations outsourcing and other services rendered to various proprietary and third party investment products and firms that may be the subject of or become associated with the services described herein.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc. Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K, NT Global Advisors, Inc., 50 South Capital Advisors, LLC, , Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.