Renato Pestana – TNT Corporation Finance Manager Americas and Asia

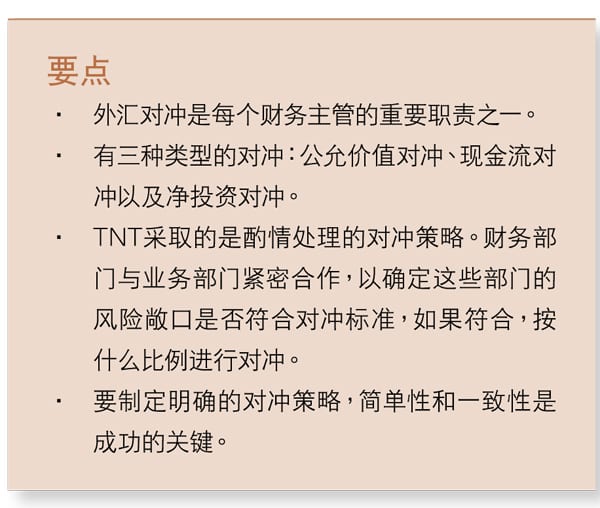

Foreign exchange hedging is one of the important responsibilities of each financial executives. If the lack of or inadequate hedging hedging financial results may fluctuate significantly. Taking into account the stakeholders’ preferences and risk management goals, develop hedging strategies is essential for the proper business. Once the deal with the foreign exchange risk of the overall attitude, treasurers can find the best approach to risk management and how to hedge operations.

Different forms of hedging

As part of the foreign exchange policy, the primary challenge is to determine when and when not to hedge to hedge. There are typically three types of hedges: fair value hedges, which involves exchange risk of net monetary assets and liabilities; cash flow hedges, which involve actual cash flows and transaction risk forecast cash flow and net investment hedges. One of the most complex commercial reasons is hedged forecast cash flow hedges and hedges of net investments in the field. According to Citigroup 2010 Citi Forex Enterprise Risk Management Survey (The survey included 307 companies), 77% of the Company’s foreign currency assets and liabilities rinse currency exchange exposure, 76% of the company’s risk exposure hedged forecast and 22 % of the company’s investment exposure rinse.

Known hedge exposure

The fair value of the hedging relates to existing financial assets and liabilities and profit and loss account which will re-valuation of financial assets and liabilities of the foreign exchange impact, therefore, to hedge commercial reasons very full. This also applies to the known transactions, such as purchase of machinery and equipment. Hedging transactions are included in the results of equity and income statement to match the cash flow occurs at the time, the initial cost of an asset or a match. Hedge accounting treatment in accordance with the effectiveness of the relevant cash flow to decide. In TNT, we have adopted a conservative approach to hedging, known commitments and net monetary assets and liabilities in foreign currency forward contracts to hedge 100%. We divided the world into developed and emerging markets. In developed markets, monetary liquidity is high, the transaction easier, we use the online forex trading platform to execute these transactions. In emerging markets, monetary liquidity is poor, and may exchange controls, we execute transactions via telephone directly with the bank.

Sign up for free to read the full article

Register Login with LinkedInAlready have an account?

Login

Download our Free Treasury App for mobile and tablet to read articles – no log in required.

Download Version Download Version

")

")

")

")