The pharma industry has historically had little need for working capital optimisation strategies, but capital released from this can be substantial. Standard Chartered’s Shoaib Yaqub, Global Head, Capital Structure Advisory, and Ashutosh Kumar, Global Head, Working Capital Solution, discuss how “pulling the right levers” could be key delivering this.

Not only has the pandemic transformed the way we live, work, travel and interact, it has also created numerous challenges for businesses around the world.

Global pharmaceutical companies are no exception; although sales of vaccines and therapeutics for Covid-19 have been an unexpected windfall for the industry, we have also seen a slowdown in research and development (R&D) and bottlenecks in the global supply chain.

With the kind of operating margins, balance sheet strength, and cash on hand that companies in other sectors could only dream of, the pharma industry has historically had little need for working capital optimisation strategies. Times are changing, however.

Over the past five years, the pharma industry’s net working capital has grown 31.4% to approximately 26% of sales. This amount of working capital could have funded approximately one third of the total capital expenditure ($181bn) during the same period.

Looking ahead, there remain numerous challenges that may stress even the most solid balance sheets, putting tied-up capital at a premium.

A competitive landscape

As drug makers respond to the pandemic by developing vaccines and therapeutics, many are losing exclusivity on blockbuster drugs over the next five years, with approximately US$236bn of sales at risk [1]. For companies that rely predominantly on prescription drug sales, replenishing the pipeline will be a crucial pillar of growth.

One way of doing this is via R&D. Already operating in an R&D intensive sector – second only to the aviation and space industry – pharma companies are set to boost R&D spend even further, especially in areas such as oncology and immunity.

While developing new products to boost growth is one option, others will look to mergers and acquisitions (M&A) to secure a more stable future, as in the case of AstraZeneca’s US$39bn acquisition of Alexion, which strengthened the British-Swedish company’s immunology offering.

According to PwC estimates, as of December 2020, the industry had 6% less capital that could be directed toward M&A versus 2019, and finding enough firepower to fuel new growth may become increasingly challenging.

Despite these pressures, investors will expect the industry to continue delivering strong returns. As sales growth normalises following a bumper 2020, pharma companies may seek to preserve the value they have created while at the same time executing new transformational strategies.

Cost-cutting measures alone are unlikely to release the levels of cash needed. However, by pulling the right levers to optimise working capital, companies can focus on their capital allocation priorities – enabling them to meet the challenges of 2021 and beyond.

A bumpy trade cycle

Research based on pharma and healthcare companies in the S&P Global 1200 Index with a market capitalisation greater than US$10bn demonstrates the different cash conversion cycle (CCC) pressures faced by companies in different geographies.

While overall, CCC days expanded in 2020 due to the impact of Covid-19 on pharma supply chains, companies in Europe and North America saw respective increases in days inventory outstanding (DIO) of four and two days as higher stock held pushed up working capital requirements. In the Asia Pacific (APAC) region, meanwhile, a days sales outstanding (DSO) increase of nine days was the main driver as conventional collection practices contributed to longer payment terms.

Source: Company Reports and Announcements, Capital IQ, SCB Analysis

Working capital levers

As the pharmaceutical industry is a capital-intensive industry characterised by big upfront costs and a lengthy wait to see a financial return, it is unlikely that drug companies can achieve similar working capital positions to the consumer goods or technology industries. Nonetheless, significant opportunities exist to unlock cash that could be productively re-invested into the business towards value generating initiatives such as R&D – without needing to put cash flows under pressure.

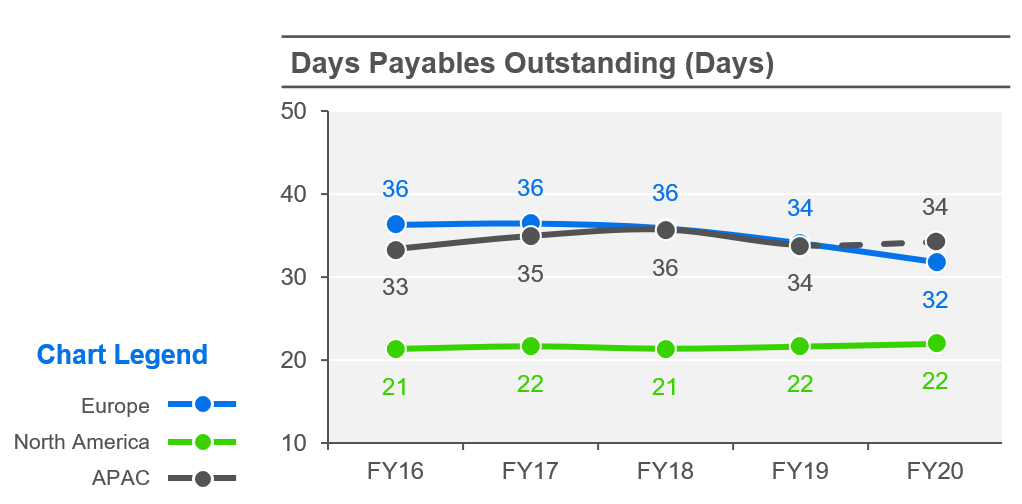

Payables

One of the most relevant working capital levers for the pharmaceutical industry today is in days payables outstanding (DPO). Compared with other industries, the average DPO in pharma is low, at 22 days for North America and 34 days across APAC and Europe. Within those figures, there is also substantial variation, with a delta of over 40 days companies in APAC. By increasing their DPO, companies can hold on to cash longer and deploy released cash where it’s needed.

Note: APAC FY20 includes LTM numbers due to timing of financial year ends

While this can be achieved by working with suppliers to extend payment terms, a preferable option is the implementation of a supply chain finance programme, which ensures suppliers have the working capital finance they need while also enabling buyers to benefit from extended payment terms.

Inventory

Global supply chains, already reeling from the US-China trade war and economic instability, have been stretched thinner still by the pandemic. This unprecedented situation challenges the “just-in-time” model, and as companies move to “just-in-case” scenarios, stock level is rising.

As companies seek to move inventory closer to their end consumers in order to guard against localised disruption within supply chains, their distributors will need working capital to take up the additional inventory. With solutions such as distributor finance, based on the strength of their relationship with the manufacturer, these distributors can receive steady and assured funding to support their working capital needs, while manufacturers save costs by converting receivables to cash on time.

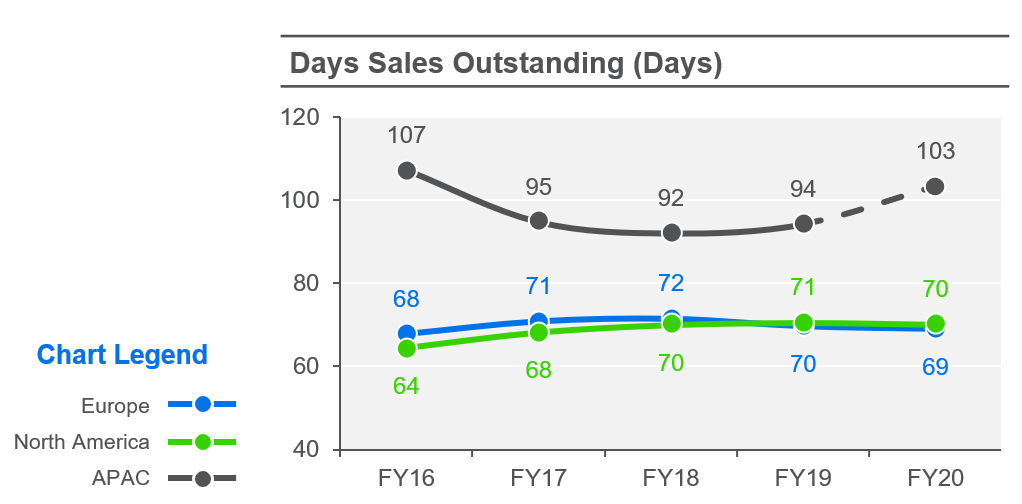

Receivables

The changes to working practices brought about by Covid-19 have stressed accounts payable processes, and this has brought about a concomitant rise in DSO. This issue is particularly acute among APAC companies, where DSO surged by nine days to 103 days in 2020 – more than 30 days greater than in Europe or North America.

For many businesses, taking control of DSO starts by automating the invoicing and collection process. This helps to reduce friction with buyers as well as increase visibility, particularly for remote teams.

To minimise DSO further, companies can also take advantage of receivables financing, thus releasing cash as well as managing the risk on their balance sheet.

Note: APAC FY20 includes LTM numbers due to timing of financial year ends

Gaining an edge

Bespoke working capital management strategies are available to help improve performance, and these have been successfully used by companies for many years.

To gain a leading edge in this challenging business environment, pharmaceutical companies have a tough task ahead. Closing the gap between sector leaders and laggards in cash conversion metrics will be vital to drive future top-line growth, and treasurers can achieve this by proactively intensifying efforts to optimise working capital, in collaboration with their banking partners.

[1] Based on Evaluate Pharma estimates in their World Preview 2020, Outlook to 2026 report

Notes

Days Sales Outstanding (DSO) = {[(Trade Receivables Beginning of Year + Trade Receivables End of Year) / 2] / Sales} x 365

Days Inventories Outstanding (DIO) = {[(Inventories Beginning of Year + Inventories End of Year) / 2] / Sales} x 365

Days Payables Outstanding (DPO) = {[(Trade Payables Beginning of Year + Trade Payables End of Year) / 2] / Sales} x 365

Cash Conversion Cycle (CCC) = DSO + DIO – DPO

")

")