by François Masquelier, Chairman, ATEL

This article discusses key strategic thoughts behind deciding when and how to hedge. It addresses the main pitfalls, inherent and new challenges as well as the education of the board and essential internal hedging reporting. It also defines the appropriate tools to face (new) accounting issues, with IAS 39 and its ‘son’ coming soon. Eventually, the OTC derivatives reform and its potential impacts on hedging strategies had to be further explained.

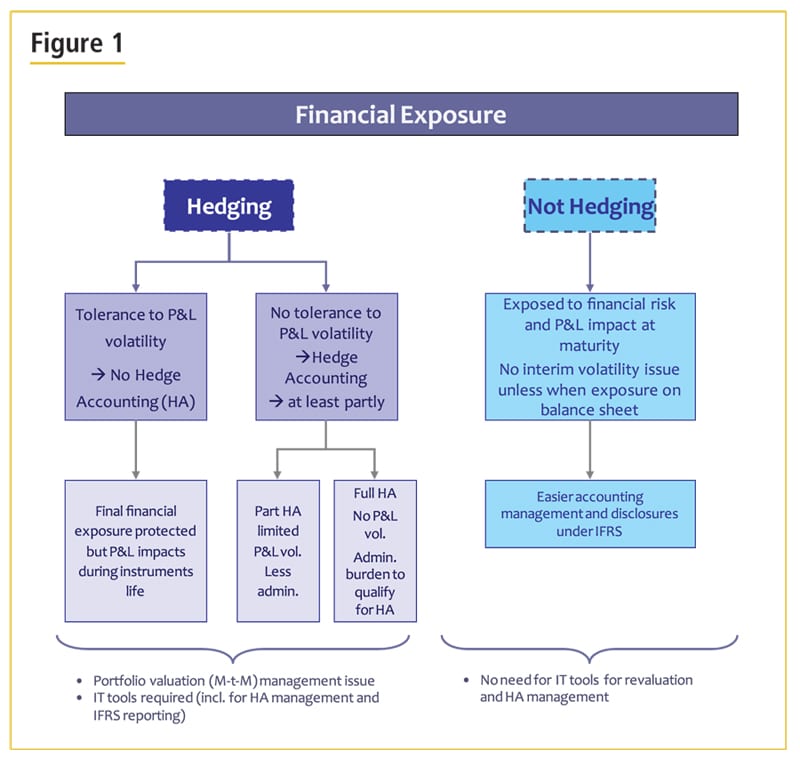

To hedge or not to hedge: that is the question

If we refer to the comments of Merton Miller, winner of the Nobel Prize in Economics in 1990 for his pioneering work in the theory of financial economics, we might conclude that hedging serves no purpose: “The most value-maximising firms do not hedge”. But can we as treasurers accept this statement at face value? Wouldn’t that amount to the negation of our profession? Even if we take into account the context of his words, and even if we accept that hedging means taking a decision and making a choice that could lead to a possible loss of opportunity, it strikes us as inadvisable to adhere purely and simply to Merton Miller’s theory (with due respect to the man and his work), as well as to his colleague Franco Modigliani.The academic issue here is whether hedging ‘creates value’. In certain cases, hedging is an obligation (contractual in the context of credits) and, in imperfect markets, sometimes makes it possible to continue to borrow. Hedging also enables treasurers to concentrate on the operational and management sides, and can create value when it sustains the company’s activity and ensures the continuity of its main aim and corporate purpose.

Non-financial companies don’t at all like speculating and remaining completely unhedged. Imagine the totality of exposure to one or more risks, such as all of the exposure to the USD, and apply to it a stress-testing factor of 20%, for example. While the CFO could live with such an impact (even if, in part, the accounting P&L result would not be affected by off-balance sheet underlying commitments), there is a high likelihood that it would not accept or tolerate such an impact, even a potential one. Just think of the amount recorded in OCI/EHR (Equity Hedging Reserve) to find out what we avoid entering in our profit and loss accounts. Thank God the IASB invented hedge accounting, to reduce the valuation to the correct level.

Sign up for free to read the full article

Register Login with LinkedInAlready have an account?

Login

Download our Free Treasury App for mobile and tablet to read articles – no log in required.

Download Version Download Version")

")

")

")