by Morten Buchgreitz, SVP and Group Treasurer, DONG Energy

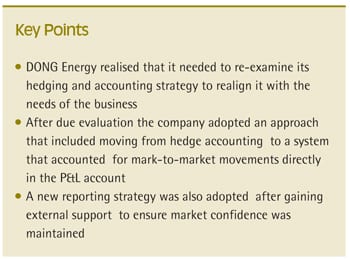

Hedge accounting under IFRS 39 or FAS 133, with future iterations, has created issues for many companies as they seek to balance the risk management needs of the business with the requirements for hedge accounting treatment. In this article, Morten Buchgreitz, SVP and Group Treasurer of DONG Energy discusses how the company made the decision to abandon hedge accounting in favour of a hedging strategy that was more closely aligned to the needs of the business, and income reporting that better reflected actual business performance.

Risk profile

As an energy company, our business is highly capital-intensive with long-term (i.e., 30-40 year) investment horizons. We therefore take a long-term view of both profitability and risk. We evaluate our exposure to a wide range of regulatory, operational, environmental and financial risks. The way that we measure and manage these risks is driven by regulation in many cases, and we also need to be sensitive to reputational and competition risk, and public and scientific opinion on issues such as climate change.

Our Group Risk Management department establishes the risk policy for the group, and consolidates reporting from across the business. Energy trading takes place in a separate department. The consolidated energy risk is transferred to them, and they manage this within defined limits. Treasury manages the remaining financial risks for which we use two systems: we use SunGard Quantum and SunGard QRisk for FX and interest rate management, Endur Openlink for energy risk management and a proprietary system for consolidated risk management.

Sign up for free to read the full article

Register Login with LinkedInAlready have an account?

Login

Download our Free Treasury App for mobile and tablet to read articles – no log in required.

Download Version Download Version")

")

")

")